There are over 100 companies that sell products that fit the definition of a wearable exoskeleton, specifically a device that is put on a person and does physical work to assist or restrict the motion between one or more joints on the human body, not just beep or vibrate. Some are marketed as “exoskeletons,” while others may be advertised as powered orthotics, rehabilitation robotics, or other catchy names.

At this point, there is no way to track the revenue of the exoskeleton industry. However, a few publicly traded companies regularly publish financial results. This is like peeping through a keyhole to try and get an understanding of what is in the room behind the door. As of last year, there were over 120 producers of exo technology. Of those, only five are publicly traded, and not all of them consider their product to be an “exoskeleton” at this time. Trying to gauge the state of the entire exoskeleton industry based on just five companies is a 1:24 ratio of publicly known revenue results to unknown revenue results.

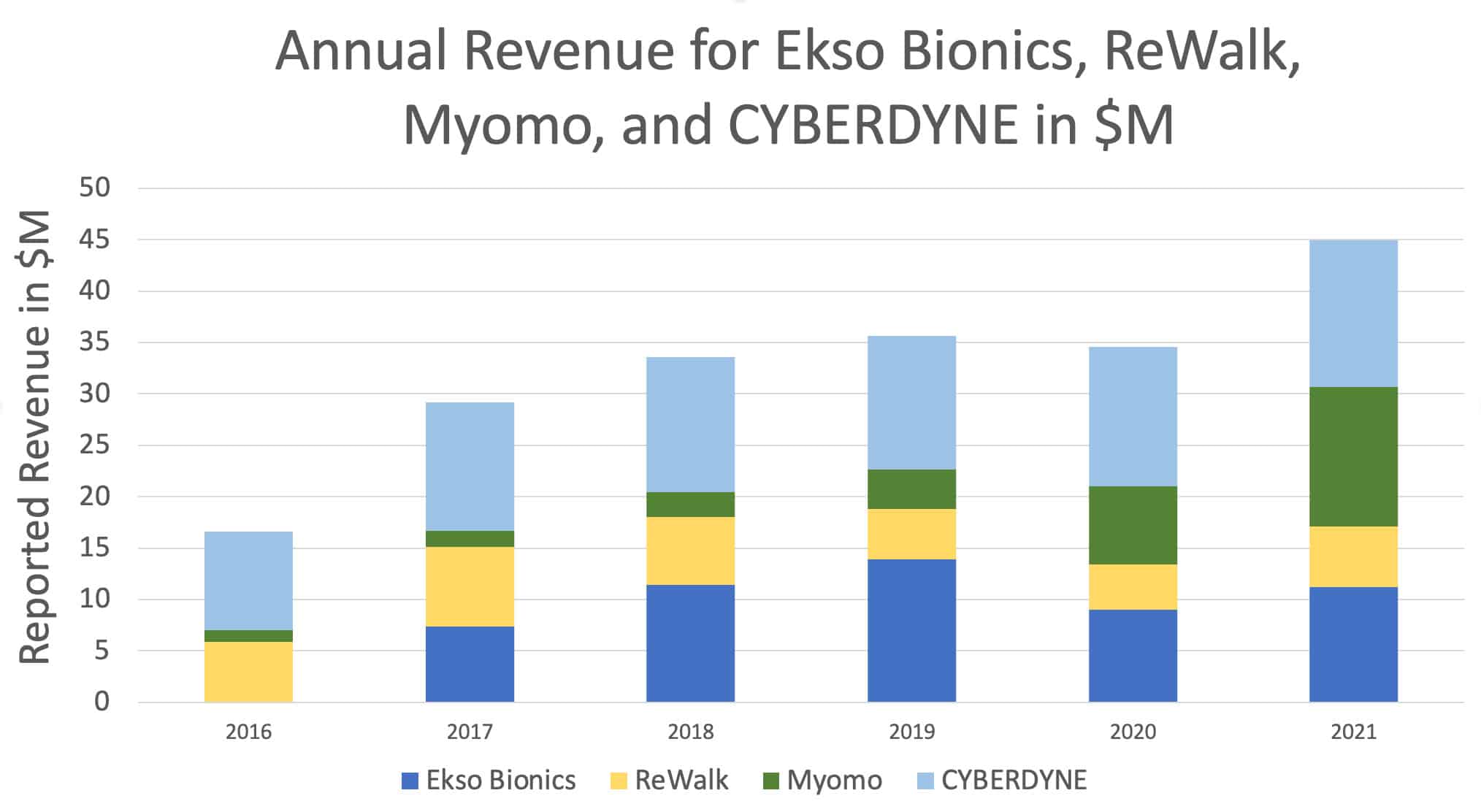

The graph above shows the reported yearly revenue for Ekso Bionics, ReWalk Robotics, Myomo, and CYBERDYNE. Note that CYBERDYNE’s fiscal year does not match the Q1 to Q4 model and therefore is shifted by several months. Also, the conversion rate of the Japanese Yen fluctuates against the US dollar, so all revenue numbers from CYBERDYNE are listed at a constant exchange rate as of the time of publishing this article. The revenue numbers for Sarcos Robotics are not included because up to 2021, the company was still working on releasing its Guardian XO full-body exoskeleton.

As discussed, the graph above represents only five out of 120+ exoskeleton developers or a 1:24 ratio. With additional information, it would have been easier to make generalized statements about the state of sales of exoskeletons. There is no evidence to be seen here of exoskeleton sales going through an exponential growth rate, but there is also no evidence that the industry is shrinking. It should be noted that the Covid-19 pandemic, which started in 2020, had a visible negative effect. The pandemic made it difficult for companies to introduce and pilot wearable devices, which require training, fitting and face-to-face time with the users. Finally, it should be noted that the company that is showing the most significant growth, Myomo, has chosen to rebrand its product to an “electronically controlled brace.”

Data:

| Year | Ekso Bionics | ReWalk | Myomo | CYBERDYNE |

| 2016 | 5.9 | 1.1 | 9.6 | |

| 2017 | 7.4 | 7.7 | 1.6 | 12.5 |

| 2018 | 11.4 | 6.6 | 2.4 | 13.1 |

| 2019 | 13.9 | 4.9 | 3.8 | 13.0 |

| 2020 | 9 | 4.4 | 7.6 | 13.6 |

| 2021 | 11.2 | 5.9 | 13.6 | 14.3 |

It would be a significant undertaking, but it would be nice to have anonymously collected data from most exoskeleton producers tracking the scale, growth, and distribution of devices and services for the entire exoskeleton industry.

Add Comment